Accounting And AI: The Impact of Artificial Intelligence and Machine Learning

Generative AI and machine learning are shaking up financial processes, making them faster, smarter, and more strategic. These tools are transforming the game — and they’re doing it fast.

But we are still in the early stages, with unprecedented growth expected. The estimated market size for AI in accounting is $6.68 billion in 2025, with a projected increase to $37.60 billion by 2030, according to data from Mordor Intelligence.

A big factor behind the accelerated growth is advances in large language models and their support of generative AI. This has introduced unprecedented scale and pre-training on diverse datasets.

Let’s take a look at the current state of AI in accounting and finance and what the future holds.

Key Takeaways

- AI is revolutionizing accounting tasks by automating repetitive processes like data entry, invoice reconciliation, and expense reporting, allowing accountants to focus on strategic, high-value activities.

- The AI in accounting market is expected to grow significantly, from $6.68 billion in 2025 to $37.60 billion by 2030, fueled by advancements in large language models and generative AI technologies.

- Adopting AI comes with challenges, including ethical considerations, data security, and ensuring responsible use of advanced technologies in financial processes.

AI in Accounting Today

The accounting industry has traditionally centered around meticulous number-crunching, complex calculations, and compliance-driven tasks. The demanding nature of this work has taken a toll on the accounting talent pipeline. Fewer students are pursuing accounting degrees, partly because the prospect of long hours spent on tedious, manual tasks is far from appealing.

However, AI is ushering in a new era where machines take on repetitive, rule-based functions, allowing accountants to focus on higher-value, strategic activities.

From automated data entry to real-time financial analysis, incorporating AI into accounting software streamlines financial processes and reduces the risk of human error.

Here are some of the major functions incorporating AI:

Efficient Invoice Processing and Reconciliation

By some estimates, incorporating accounting AI into e-invoicing will save up to $28 billion in the next 10 years.

If that number is too big to wrap your head around, consider how many hours an AP team spends reconciling transactions with invoices.

AI technologies, particularly optical character recognition (OCR) and machine learning (ML) algorithms, are pivotal in streamlining invoice processing.

How exactly does AI simplify this process?

- Easy data extraction. OCR extracts relevant information from invoices, including invoice numbers, dates, line items, and amounts. AI automatically assigns transactions a category based on past behavior.

- Automatic tagging. Transactions are coded, tagged, and recorded in the general ledger automatically. This eliminates the need for manual data entry, reducing the likelihood of human errors and accelerating the overall processing time.

- Touchless AP. Users can choose to have invoice details coded at the line level by vendor or summarize the bill into one line item after the invoice is scanned. Generative AI and ML automatically populate the description and category, improving accuracy with every transaction.

- Smart reconciliation. Through pattern recognition and data analysis, AI systems can swiftly identify discrepancies and exceptions, flagging them for further review by human accountants. This expedites the reconciliation process and enhances accuracy by minimizing the risk of oversight.

In essence, AI transforms invoice processing and reconciliation from time-consuming manual tasks to efficient, accurate, and automated accounting processes that contribute to overall financial transparency and integrity.

Touchless Expense Reporting

Nobody likes filling out expense reports. Now, technology can take over that often-procrastinated task.

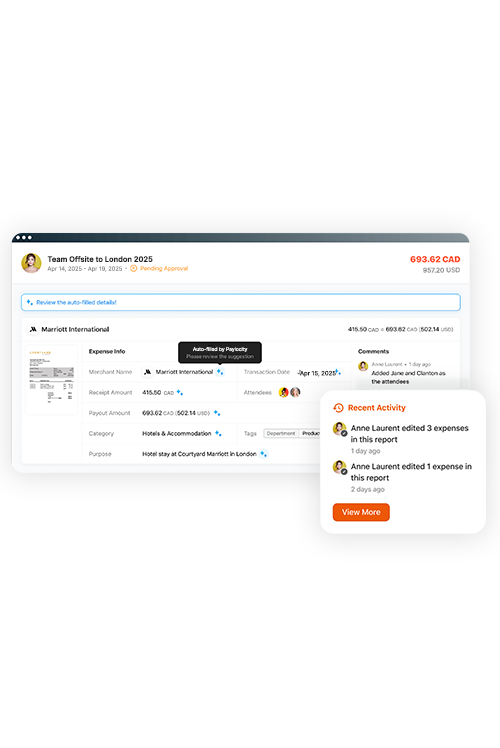

AI allows employees to simply take a photo of a receipt in the mobile app or submit it through a dedicated receipt inbox. The accounting technology takes it from there, automatically populating expense request details using the latest OCR technology. Built-in ML extracts the relevant information, including GL category, date, amount, and vendor, and generative AI fills in the purpose based on past patterns.

Fraud Detection

AI can analyze vast amounts of data far faster than any human.

The ability to simultaneously analyze financial data from diverse sources, including transaction history, user behavior, and external data feeds, empowers accounting professionals to uncover subtle signs of fraudulent activity that may escape human eyes. Suspicious transactions can be instantly flagged for further investigation.

AI is trained on historical fraud cases, so its detection skills are continuously evolving.

Budgeting and Forecasting

AI in financial planning and analysis (FP&A) empowers data-driven decisions and helps organizations navigate complex financial forecasting with agility and precision.

By analyzing large datasets, AI can provide insights into market conditions, competitive landscapes, and other factors that affect planning and strategy.

Machine learning algorithms enable more accurate forecasting by analyzing historical data and identifying patterns and variables. This predictive capability supports accurate scenario planning and risk assessment.

AI-driven automation also takes over manual, routine accounting tasks like data entry and report generation so that the FP&A team can focus on strategic analysis.

Document Intelligence

AI can instantly identify key information from order forms and Service Organization Controls (SOC) documents to save time and improve accuracy. When built into intake workflows, AI extracts crucial data such as payment terms, auto-renewals, and pricing details. In Paylocity, generative AI prefills all of these purchasing details and GL links to reduce manual data entry.

AI can also scan SOC documents to detect and highlight potential exceptions and tested controls so approvers can efficiently review and manage related purchase requests within existing workflows.

Back-Office Functions

Back-office functions are the administrative and support tasks critical to a company’s operations, including data entry, processing, payroll, and compliance activities. AI helps automate these repetitive tasks to save time.

But AI’s impact on back-office functions extends beyond mere task automation; it introduces a paradigm shift by leveraging continuous learning from historical data.

These systems evolve to handle intricate tasks that conventionally necessitate human intervention. AI then minimizes the inherent risk of errors in manual work, elevating the overall accuracy and efficiency of back-office business processes everywhere.

By harnessing AI’s ability to learn from experience, organizations benefit from streamlined operations, reduced reliance on repetitive manual efforts, and an enhanced ability to navigate complex and dynamic business environments.

Automating Bookkeeping Tasks

Many bookkeeping and accounting tasks can be taken over by AI, including:

- Categorizing transactions

- Reconciling transactions

- Data entry, including extracting information from receipts and invoices

- Identifying errors and discrepancies in financial data

It’s often said that AI will elevate the accounting profession by freeing up more time to focus on more rewarding value-added activities.

Bookkeepers, on the other hand, do face declining job prospects. They can protect their career path by developing soft skills such as critical thinking, problem-solving, and effective communication. This can distinguish them in roles that require a human touch, such as client interactions and strategic financial advisory services.

Proactively learning to integrate AI tools into their skill set can further enhance job security.

10 Benefits of Using AI in Accounting and Finance

It’s a brave new world for finance and accounting professionals. As accounting AI advances rapidly, here are some of the advantages.

- Automation of routine tasks. AI in accounting software automates mundane and repetitive tasks such as data entry, invoice processing, and transaction categorization, freeing up time for accountants to focus on more strategic activities.

- Enhanced accuracy. Machine learning algorithms improve the accuracy of financial analysis by reducing the risk of human errors associated with manual data entry and calculations.

- Efficient data processing. AI can quickly analyze vast amounts of financial data, providing faster insights into trends, anomalies, and potential risks.

- Real-time monitoring. AI technology enables real-time financial transaction monitoring, helping promptly identify and address issues, anomalies, or fraudulent activities.

- Improved decision-making. By providing data-driven insights and predictions, AI accounting software enhances the decision-making process for financial planning, budgeting, and strategic financial management.

- Cost savings. Automation through AI leads to cost savings for accounting firms and businesses by reducing the need for manual labor and minimizing the risk of financial errors.

- Adaptive learning. Machine learning models can continuously learn and adapt to evolving financial patterns, ensuring that the accounting systems remain up to date and effective.

- Enhanced fraud detection. AI technology helps in the early detection of fraudulent activities by analyzing patterns, anomalies, and deviations in financial transactions.

- Streamlined compliance. AI accounting software assists in navigating complex regulatory landscapes by automating compliance checks and ensuring that your business’s financial health, financial statements, and records adhere to the latest regulations.

- Increased productivity. By automating routine tasks, accountants can focus on high-value activities, leading to increased productivity and improved client services.

Challenges of Adopting AI in Accounting and Finance

Despite the many advantages, incorporating AI in accounting is not without challenges. Here's how to tackle those challenges head-on and make the case for AI efficiency.

Hesitance Around New Technology

A 2024 Thomas-Reuters survey revealed that 79% of accounting firms have no plans to adopt generative AI technology or are still considering it.

One significant hurdle is the resistance often encountered within traditional accounting practices. Accountants may question the reliability of AI accounting software, particularly in areas requiring nuanced judgment or interpretation.

How to Overcome the Challenge

Focus on education, transparency, and gradual integration. Offering training programs and workshops can help accountants and finance teams build confidence in using AI tools, enabling them to understand how these technologies can complement rather than replace their expertise.

Organizations should prioritize transparency by clarifying how AI systems make decisions and ensuring compliance with relevant regulations. Starting with small pilot projects can also ease the transition, allowing firms to evaluate the benefits and address concerns on a smaller scale before implementing AI across broader operations.

Technical and Talent Requirements

Another challenge is the need for significant investments in technology infrastructure and talent.

Implementing accounting AI systems requires a robust technological framework, including high-performance computing, data storage, and cybersecurity measures.

Additionally, organizations need skilled personnel who can develop, deploy, and maintain AI solutions. The shortage of AI talent in the job market further exacerbates this challenge.

How to Overcome the Challenge

Prioritize scalable and cloud-based solutions that reduce upfront costs while ensuring flexibility for future growth. Implement partnerships with tech providers to access cutting-edge tools without requiring complete in-house development.

To tackle the shortage of skilled AI talent, organizations can focus on cultivating internal talent by offering training programs and fostering a learning culture. Collaboration with universities and educational institutions to create specialized programs may help build a sustainable pipeline of skilled professionals.

Ethical Considerations

Integrating AI into existing accounting processes also demands careful consideration of ethical and regulatory implications, addressing data privacy, security concerns, and potential biases in AI algorithms.

How to Overcome the Challenge

Establish clear guidelines and frameworks for the ethical use of AI, ensuring compliance with data privacy regulations and mitigating biases in AI algorithms. Regular audits and monitoring of AI systems can reinforce accountability and transparency.

Also, fostering strong collaboration with technology providers and industry peers can support sharing best practices, ensuring organizations remain agile and adaptive to emerging trends.

Security Concerns

The use of sensitive financial data raises questions about how this information is handled, stored, and protected.

Organizations must implement robust data privacy measures to safeguard against potential breaches, ensure compliance with stringent data protection regulations, and foster trust among clients and stakeholders.

How to Overcome the Challenge

Adopt a multi-layered approach to data protection. This includes implementing advanced encryption techniques to secure sensitive financial information during storage and transmission. Regularly updating security protocols and conducting thorough vulnerability assessments helps systems remain resilient to emerging threats.

Additionally, foster a culture of cybersecurity awareness through employee training to mitigate risks stemming from human error. Collaborate with cybersecurity experts and invest in cutting-edge technologies, such as AI-driven threat detection, to enable proactive identification and response to potential issues.

Will AI Replace Accountants?

While AI is poised to transform the accounting and finance industry, it is unlikely to replace accountants completely.

Instead, AI will augment finance work by automating repetitive tasks such as data entry, transaction categorization, and basic reporting. This allows accountants to focus on higher-value activities, including strategic planning, financial analysis, and personalized client advice.

Furthermore, accounting requires a deep understanding of complex regulations, ethical considerations, and the ability to make nuanced judgments — areas where human expertise remains essential. Rather than replacing accountants, AI is more likely to serve as a powerful tool that enhances their efficiency and decision-making capabilities.

Stop Uncontrolled Spend with Paylocity for Finance

Optimize your company’s spend management with Paylocity for Finance. Get real-time visibility, faster financial close, improved planning, and stronger financial controls.

Related