Affordable coverage (ACA)

Summary definition: Under the Affordable Care Act, an employer healthcare plan whose lowest-cost option is below a set percentage of household income.

What is affordable coverage?

Affordable coverage is an Affordable Care Act (ACA) compliance standard employers must meet to demonstrate the relative cost of their provided healthcare plans. It’s based on the maximum percentage of household income an employee would have to spend on a plan's least expensive options.

For 2027 calendar year plans, the plan is deemed affordable if its least expensive self-care option is less than 10.22% of a household’s income. This is an increase from the 2026 rate of 9.96%. Furthermore, employers must demonstrate that their overall company plan would cover a minimum value of at least 60% of expected employee medical costs.

Applicable large employers (ALEs) who don't meet these standards could be subject to IRS tax penalties that help fund healthcare subsidies.

Passed in 2010, the ACA introduced significant reforms to the healthcare landscape. The law created marketplaces for health insurance, expanded Medicaid eligibility, and prevented insurers from refusing to provide coverage because of pre-existing conditions.

Key takeaways

- Affordable coverage under the ACA is determined by a maximum percent of household income employees would have to spend on the lowest-cost employer healthcare option.

- Employers must demonstrate that their coverage is affordable using one of three safe harbor methods. Qualifying health plans must also be shown to cover at least 60% of anticipated healthcare costs for a collective workforce.

- Employers not meeting affordability or minimum value standards may be subject to “employer-shared responsibility” payments to the IRS.

Affordability safe harbors

Since employers don’t have access to complete household income (given there may be multiple income sources), the Internal Revenue Service (IRS) provides three affordability safe harbors to serve as proxies. Each has advantages and disadvantages for different types of employers:

- W-2 Box 1 Wages Safe Harbor: Under this method, the monthly premium for self-only coverage must not exceed 10.22% of the employee's W-2 Box 1 wages, which is the employee's gross income minus pre-tax deductions. The coverage must be affordable for all the months the employee is eligible.

- Federal Poverty Line (FPL) Safe Harbor: This method uses the FPL as its baseline, which is adjusted annually based on the cost of living. To qualify, the monthly premium for self-only coverage must not exceed 9.96% of the FPL for the employee's household size and geographic area.

- Rate of Pay Safe Harbor: This method uses an employee’s regular pay rate to gauge affordability. To qualify, the monthly premium for self-only coverage must not exceed 10.22% of either:

- the employee's lowest hourly pay rate multiplied by 130 hours

- the employee's monthly salary (provided it wasn't reduced during the year)

Specific rules and regulations related to the ACA may change over time, so you should consult legal or regulatory experts before deciding which method to use.

Minimum value standard

Along with the affordability threshold, the ACA established a minimum value standard for employer-sponsored health plans, ensuring that employers offer comprehensive plans that cover a wide range of services.

This standard requires employer-provided health plans to cover at least 60% of their workforce’s expected medical costs, such as doctor visits, hospital stays, and prescription drugs.

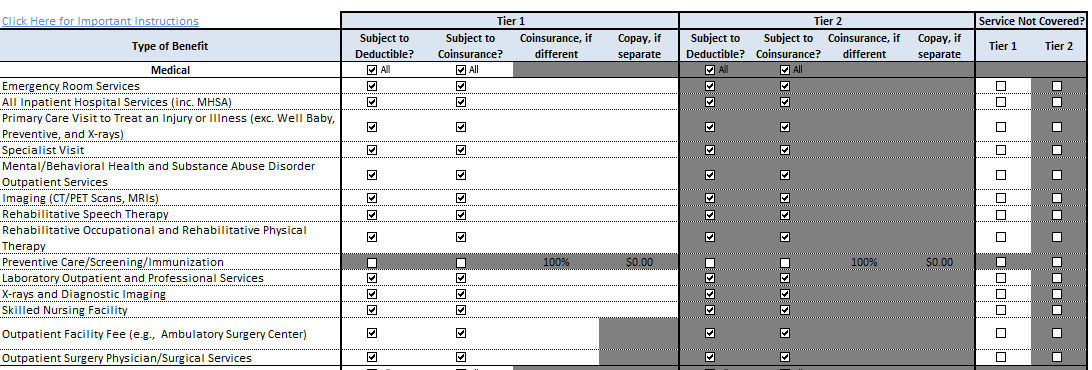

To help employers assess if their plans meet this requirement, the Centers for Medicare & Medicaid Services (CMS) downloadable minimum value calculator asks questions regarding deductibles and copays for various medical services under the plan.

An image of the HHS’s minimum value calculation, which employers can use to determine whether their health plan meet ACA coverage standards.

An image of the HHS’s minimum value calculation, which employers can use to determine whether their health plan meet ACA coverage standards.

Plans that don’t meet the 60% minimum value standard are not considered to provide minimum essential coverage (MEC) under the ACA. Employees offered such a plan may be eligible for subsidies to help them buy coverage on the Health Insurance Marketplace.

ACA non-compliance penalties

Employers who fail to demonstrate affordability and minimum value under the ACA may be subject to two types of penalties called “employer-shared responsibility payments.” This failure is most readily identified when a full-time employee receives a premium tax credit for a healthcare marketplace despite being enrolled in their employer's plan. If this happens, it triggers a 4980(H) penalty, which includes the following amounts for 2026:

- 4980H(a) Penalty - If the employer fails to offer coverage or offers it to less than 95% of its full-time employees and their dependents, they're fined $3,340 annually per full-time employee (minus the first 30 employees).

- 4980H(b) Penalty - If the employer offers coverage that isn't "affordable" or doesn't have "a minimum value", they're fined 1/12 of $5,010 (i.e., $417.50) per employee who received a tax credit that month for each month there’s a violation.

Note, if an organization may be penalized under both provisions, the amount is capped at what can be assessed under 4980H(a).

Employers should review IRS safe harbor guidance and speak to a trusted legal advisor for additional guidance. Previous penalty amounts are provided on the IRS website.

Optimize your benefits experience

Help your employees get the most out of their benefits while getting time back in your day through smart automation. With all-in-one tools, kicking off open enrollment and administering third-party benefits services like FSAs, HSAs, and more is a breeze! And employee experience features like integrated training and expert groups, all available on the go, ensure your employees are making informed decisions.